If you have student loans, you know how your debt can affect your ability to pursue your other financial goals, especially saving for retirement. According to a recent survey by TIAA, 84% of responding adults said that their student loans negatively impacted the amount they were able to save for retirement. For those who aren’t saving for retirement at all, 26% said their student loan balances were why they couldn’t afford to do so. However, putting off saving for your retirement is a costly mistake. It’s important to balance saving for your future with paying down student loan debt now. If you’re struggling to manage both priorities, here’s how to save for retirement while keeping up with your loan payments.

Why you need to save for retirement now

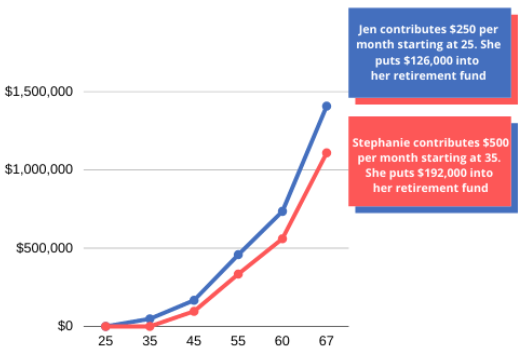

When it comes to saving for retirement, the earlier you begin saving, the better. Compound interest and the power of annual returns can help your money grow over time. The longer you wait to start saving for retirement, the more you’ll have to invest your own money to have enough saved to retire comfortably. For example, let’s say Jen begins saving for retirement at the age of 25. She contributes $250 per month into her retirement account, and her average annual return is 9%. By the time Jen reaches the age of 67, she’s contributed just $126,000 into the account, but her retirement account is worth $1,406,746. By contrast, Jen’s friend Stephanie puts off saving for retirement until she pays off her student loans and doesn’t start contributing to her retirement until she’s 35. She starts putting $500 per month toward her retirement fund — double what Jen contributes each month. Like Jen, Stephanie earns an average annual return of 9%, but by the age of 67, her retirement fund is worth only $1,108,257. Stephanie contributed $192,000 of her own money — nearly $70,000 more than Jen — but her retirement account is worth approximately $300,000 less than Jen’s because Stephanie got a later start.

Retirement savings options

If you’re not sure how to save for retirement, here are some popular retirement plans.

401(k)

A 401(k) plan is an employer-sponsored retirement plan, meaning it’s a benefit offered through your job. With a 401(k), you invest a portion of your pre-tax salary in the investments you choose. Your contributions and the earnings are not taxed until you withdraw from the account.

401(3)b

401(3)b plans are very similar to 401(k) plans, but they’re offered to employees of non-profit organizations, churches, public schools, and universities. You make contributions to your retirement plan on a pre-tax basis, and your contributions and earnings aren’t taxed until you make withdrawals.

IRAs

Another great option is to open an Individual Retirement Account (IRA) on your own. There are two options: a Traditional IRA and a Roth IRA.

Traditional IRA

Anyone can contribute to a Traditional IRA, regardless of income. With an IRA, your earnings can grow tax-deferred, meaning you only pay taxes on your gains when you make withdrawals in retirement. Your contributions may be tax-deductible depending on your income level and if you have access to an employer-sponsored plan.

Roth IRA

If you meet the income restrictions, a Roth IRA may be a useful option. With a Roth IRA, you make contributions with after-tax dollars. Why is that a good thing? While your contributions aren’t tax-deductible, your earnings and withdrawals are tax-free. And, you can take out the money you contribute to your Roth IRA — but not your earnings — before you reach retirement age without paying any penalties, so your Roth IRA can double as an emergency fund in a pinch.

How to save for retirement while paying student loans

Finding a balance between saving for retirement and paying down student loan debt can be tricky, but it can be done if you follow these three steps:

1. Make the minimum payments on all of your student loans

It’s important to stay current on all of your debt to maintain and protect your credit score and prevent racking up costly late fees. Keep making all of the required minimum payments on your federal and private student loans to avoid falling behind and entering student loan default.*

2. If your employer offers matching contributions, contribute enough to earn the full match

If you have access to an employer-sponsored retirement plan like a 401(k) or 403(b) and your employer offers matching contributions, contribute enough to your account to qualify for the full match. Otherwise, you’ll lose out on free money that is a key part of your compensation package. Over time, skipping the match could cost you thousands of dollars. For example, let’s say you make $40,000 per year, and your employer will match 100% of your contributions, up to 5% of your salary. That means if you contribute $2,000 per year to your retirement plan — 5% of your salary — your employer will match your contribution, giving you an additional $2,000 per year toward your retirement fund. If you didn’t take advantage of the match while you were with that employer for five years, you’d miss out on $10,000. But the long-term consequences are even worse. If that money earned an average 9% annual return, in 30 years, that $10,000 would be worth over $147,000. That’s why it’s so important to take advantage of employer matching contributions if they’re available to you. If your employer doesn’t offer a match, or if you don’t have access to an employer-sponsored plan, contribute to a Traditional IRA or Roth IRA instead.

3. Tackle your high-interest student loan debt

If you have extra money left over each month, put it toward high-interest student loan debt, meaning loans with an interest rate of over 5%. You can also consider student loan refinancing to lower your interest rate and reduce your monthly payment. By refinancing your student loans, you can save money and free up more money in your monthly budget to save for retirement. Use the student loan refinance calculator to see how much you can save.*

The bottom line

When it comes to saving for retirement while paying student loans, you should develop a balanced strategy. Aim to both save for retirement and pay down your student loans at the same time. By taking advantage of employer contributions and tackling high-interest debt, you can improve your finances and build a secure future.

*Subject to credit approval. Terms and conditions apply. Notice About Third Party Websites: Education Loan Finance by SouthEast Bank is not responsible for and has no control over the subject matter, content, information, or graphics of the websites that have links here. The portal and news features are being provided by an outside source – the bank is not responsible for the content. Please contact us with any concerns or comments.